Appealing a Denied Claim: Your Options and Rights

Understanding Car Insurance Claim Denials and Your Appeal Rights

So, you got that dreaded letter – claim denied. Bummer, right? But don't throw in the towel just yet. Insurance companies deny claims all the time, and sometimes it's a mistake, sometimes it's a misinterpretation, and sometimes... well, okay, sometimes they're hoping you'll just go away. But you don't have to. You have rights, and you have options for appealing that denied car insurance claim. This section dives into the common reasons for denials and the legal basis for your appeal.

Common Reasons for Car Insurance Claim Denials

First things first, let's figure out why they said no. Here are some of the usual suspects:

- Policy Lapses: Did you forget to pay your premium? A lapsed policy means no coverage. Always double check your payment status.

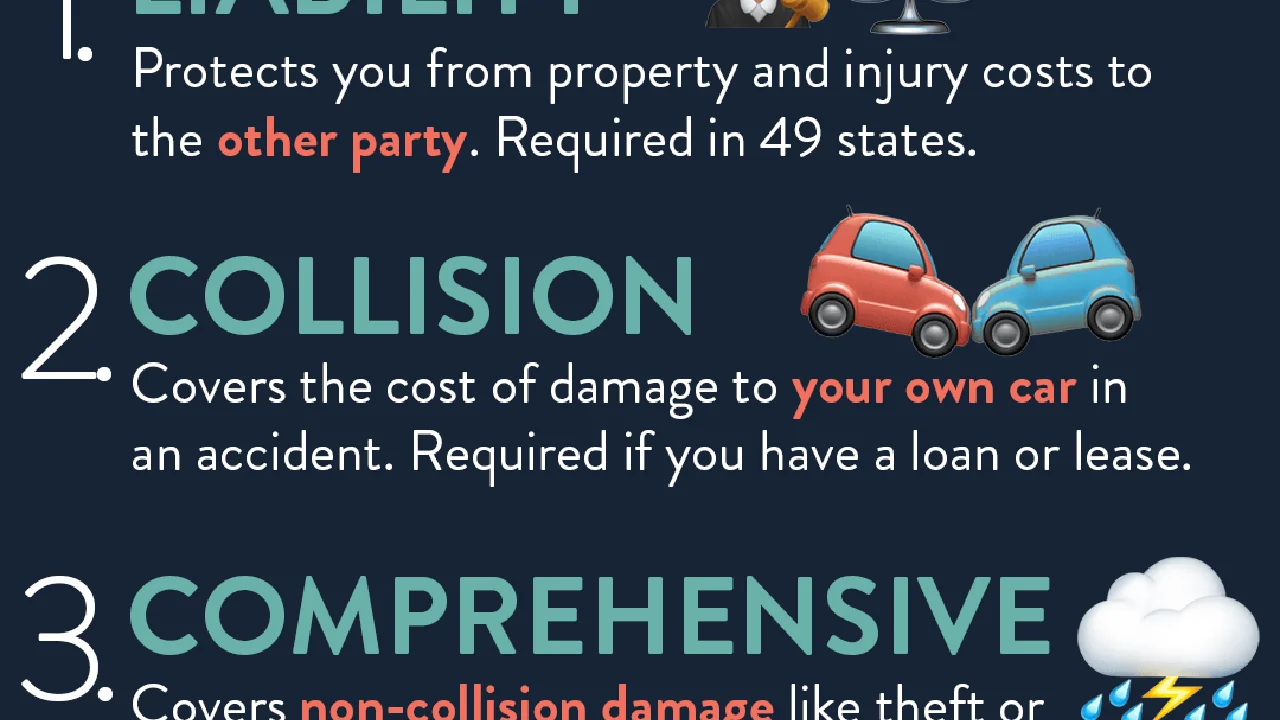

- Exclusions: Every policy has exclusions. Maybe you were using your car for something your policy doesn't cover (like ridesharing if you didn't disclose it). Or maybe the damage was caused by something specifically excluded, like an earthquake (depending on your policy and location). Read the fine print, folks.

- Disputed Liability: The insurance company might disagree about who was at fault in the accident. This is a big one, and often requires investigation.

- Insufficient Evidence: Maybe you didn't provide enough documentation to support your claim. Photos, police reports, witness statements – they all help.

- Fraudulent Claims: Insurance companies are always on the lookout for fraud. If they suspect you're lying or exaggerating, they'll deny the claim faster than you can say "deductible."

- Coverage Limits Exceeded: Your damage might exceed your policy's limits. If you only have $10,000 in property damage liability and you totaled a Lamborghini, you're going to be paying the difference out of pocket.

Your Legal Rights When Appealing a Claim Denial

Good news: you're not powerless. You have the right to appeal the decision. Here's the gist:

- Review Your Policy: This is crucial. Know what your policy covers, what it excludes, and what the claims process is.

- Document Everything: Keep records of all communication with the insurance company, including dates, times, and names of people you spoke with.

- Understand State Laws: Insurance regulations vary by state. Familiarize yourself with your state's laws regarding insurance claims and appeals. Your state's Department of Insurance is a great resource.

- Right to an Independent Review: In some cases, you can request an independent review of your claim by a third party.

- Consider Legal Counsel: If the claim is substantial or the denial seems unfair, talk to an attorney specializing in insurance claims.

Gathering Evidence for Your Car Insurance Claim Appeal and Strengthening Your Case

Think of your appeal as a mini-trial. You need to present a strong case. That means gathering evidence and building a compelling argument.

Essential Documents for Your Appeal

- The Denial Letter: This is your starting point. Carefully read the letter to understand the reason for the denial.

- Your Insurance Policy: Have it handy and refer to specific clauses that support your claim.

- Police Report: If the accident was reported to the police, get a copy of the report.

- Photos and Videos: Photos of the damage to your car, the other vehicle, and the accident scene are invaluable. Video footage (dashcam, security cameras) is even better.

- Witness Statements: If there were witnesses to the accident, get written statements from them.

- Repair Estimates: Get estimates from reputable auto body shops. Multiple estimates are even better.

- Medical Records: If you were injured in the accident, gather your medical records and bills.

- Expert Opinions: If the denial is based on a technical issue (e.g., the cause of the accident), consider getting an expert opinion from an accident reconstruction specialist.

Crafting a Compelling Appeal Letter

Your appeal letter is your chance to directly address the insurance company and explain why their denial was wrong. Here's how to write a persuasive one:

- Be Clear and Concise: State the purpose of your letter – you are appealing the denial of your claim.

- Reference the Claim Number: Include your claim number and policy number.

- Address the Specific Reason for Denial: Directly address the reason the insurance company gave for denying your claim.

- Present Your Evidence: Clearly and logically present the evidence that supports your claim. Refer to specific documents (e.g., "As shown in the police report...").

- Cite Relevant Policy Provisions: Refer to specific sections of your insurance policy that support your claim.

- Be Professional and Respectful: Even if you're frustrated, maintain a professional tone. Avoid personal attacks or accusatory language.

- State Your Desired Outcome: Clearly state what you want the insurance company to do – overturn the denial and pay your claim.

- Set a Deadline: Give the insurance company a reasonable deadline to respond to your appeal.

Navigating the Car Insurance Claim Appeal Process and Timelines

The appeal process can vary depending on your insurance company and your state. Knowing what to expect can help you stay on track and avoid delays.

Understanding the Insurance Company's Internal Appeal Process

Most insurance companies have an internal appeal process. This usually involves submitting your appeal letter and supporting documentation to a specific department within the company. The company will then review your appeal and make a decision. This process can take several weeks or even months.

Deadlines for Filing an Appeal

Pay close attention to the deadlines for filing an appeal. These deadlines are usually stated in your insurance policy or in the denial letter. Missing the deadline could mean losing your right to appeal. If you're unsure about the deadline, contact your insurance company or an attorney.

Escalating Your Car Insurance Claim Appeal Beyond the Insurance Company

What if the insurance company denies your appeal? Don't give up! You have other options.

- State Department of Insurance: You can file a complaint with your state's Department of Insurance. The department will investigate your complaint and may be able to help you resolve the dispute.

- Mediation: Mediation is a process where a neutral third party helps you and the insurance company reach a settlement.

- Arbitration: Arbitration is a more formal process where a neutral third party hears evidence and makes a binding decision.

- Lawsuit: As a last resort, you can file a lawsuit against the insurance company. This is a serious step, and you should consult with an attorney before taking it.

Specific Products and Scenarios for Car Insurance Claim Appeals

Let's get specific. Here are some real-world scenarios where appealing a denied claim is crucial, along with some product recommendations that can help your case.

Scenario 1: Disputed Liability After a Car Accident with Bodily Injury

Imagine you're involved in a car accident where the other driver claims you were at fault, even though you believe they were. They have injuries, and their insurance company denies your claim, arguing you caused the accident. This is a high-stakes situation because bodily injury claims can be very expensive. In this case, you'll need to build a strong case proving the other driver's negligence.

Product Recommendations:

- Dash Cam (Vantrue N4 Pro): A high-quality dash cam that records front, rear, and interior views simultaneously. The Vantrue N4 Pro offers excellent video quality, even at night, and can provide crucial evidence in a disputed liability case. Use Case: Capturing the accident as it happened, proving who ran the red light, or showing the other driver's reckless behavior. Comparison: Compared to cheaper dash cams, the Vantrue N4 Pro offers superior video quality and reliability. While the upfront cost is higher (around $300), the potential benefit in a disputed claim is well worth it. Cheaper cameras might have blurry footage or fail to record crucial moments. Price: Approximately $300.

- Accident Reconstruction Software (Virtual CRASH): This software is used by accident reconstruction experts to simulate accidents and determine the cause. While you probably won't buy this yourself, knowing it exists is helpful. Use Case: Hiring an accident reconstruction expert who uses this software can create a visual representation of the accident, demonstrating the other driver's fault. Comparison: Virtual CRASH is considered one of the most accurate and comprehensive accident reconstruction software programs available. Price: Software license fees are substantial (thousands of dollars), so this is an expert service.

Scenario 2: Totaled Car and Disagreement on Fair Market Value

Your car is totaled in an accident. The insurance company offers you what you believe is a ridiculously low settlement based on the car's "fair market value." They're lowballing you, hoping you'll accept the first offer. This is a common tactic. You need to prove your car was worth more than they're offering.

Product Recommendations:

- Vehicle Valuation Tools (Kelley Blue Book, Edmunds): These online tools provide estimates of your car's value based on its make, model, year, mileage, and condition. Use Case: Gathering multiple valuations from different sources to demonstrate that the insurance company's offer is too low. Print out the reports and include them in your appeal letter. Comparison: Kelley Blue Book is generally considered the industry standard, but it's a good idea to check Edmunds and other sources as well. Each site may use slightly different methodologies, resulting in different valuations. Price: Free to use for basic valuations.

- Independent Appraisal (Local Auto Appraiser): A professional auto appraiser can provide a written appraisal of your car's value based on a physical inspection. Use Case: Providing a more accurate and detailed valuation of your car, especially if it has unique features or upgrades. Comparison: An independent appraisal is more credible than online valuations because it's based on a physical inspection. Price: Typically ranges from $200 to $500.

Scenario 3: Denied Claim Due to a Pre-Existing Condition

Your car is damaged, and the insurance company claims the damage was caused by a pre-existing condition and therefore isn't covered. For example, they might argue that the rust on your car was there before the accident and contributed to the damage. You need to prove that the damage was directly caused by the accident, not by the pre-existing condition.

Product Recommendations:

- Professional Auto Body Shop Inspection (Reputable Local Shop): A detailed inspection from a reputable auto body shop can determine the extent of the damage caused by the accident versus any pre-existing conditions. Use Case: Obtaining a written report from the auto body shop that clearly distinguishes between the new damage and any pre-existing damage. Comparison: Choose a shop with a good reputation and experience in handling insurance claims. Get multiple opinions if possible. Price: Inspection fees vary, but typically range from $50 to $150.

- Before-and-After Photos (Personal Archive): If you have photos of your car taken *before* the accident, they can be invaluable in proving the extent of the new damage. Use Case: Comparing the before-and-after photos to show the specific damage caused by the accident and refute the insurance company's claim of pre-existing conditions. Comparison: Before-and-after photos are powerful visual evidence that can be difficult for the insurance company to dispute. Price: Depends on if you need to develop older photos.

Leveraging Technology in Your Car Insurance Claim Appeal

Technology can be your friend in the appeal process. Here are some tech tools that can help.

- Smartphone Apps for Accident Documentation: Apps like "Accidentally" and "Crash Report" can help you document the accident scene, gather information, and create a report.

- Cloud Storage for Secure Document Management: Use cloud storage services like Google Drive or Dropbox to securely store all your documents related to your claim.

- Online Legal Resources: Websites like Nolo.com provide information about insurance law and your rights.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)