The Role of Deductibles in Car Insurance

Understanding Car Insurance Deductibles What They Are and Why They Matter

Okay, so you're diving into the wonderful world of car insurance. First off, good for you! Being informed is the best way to save money and avoid nasty surprises later. One term you're going to hear a lot is "deductible." Simply put, a deductible is the amount of money you pay out-of-pocket before your insurance company kicks in to cover the rest of the damages in a covered claim. Think of it like this: you and your insurance company are splitting the bill. Your deductible is your share.

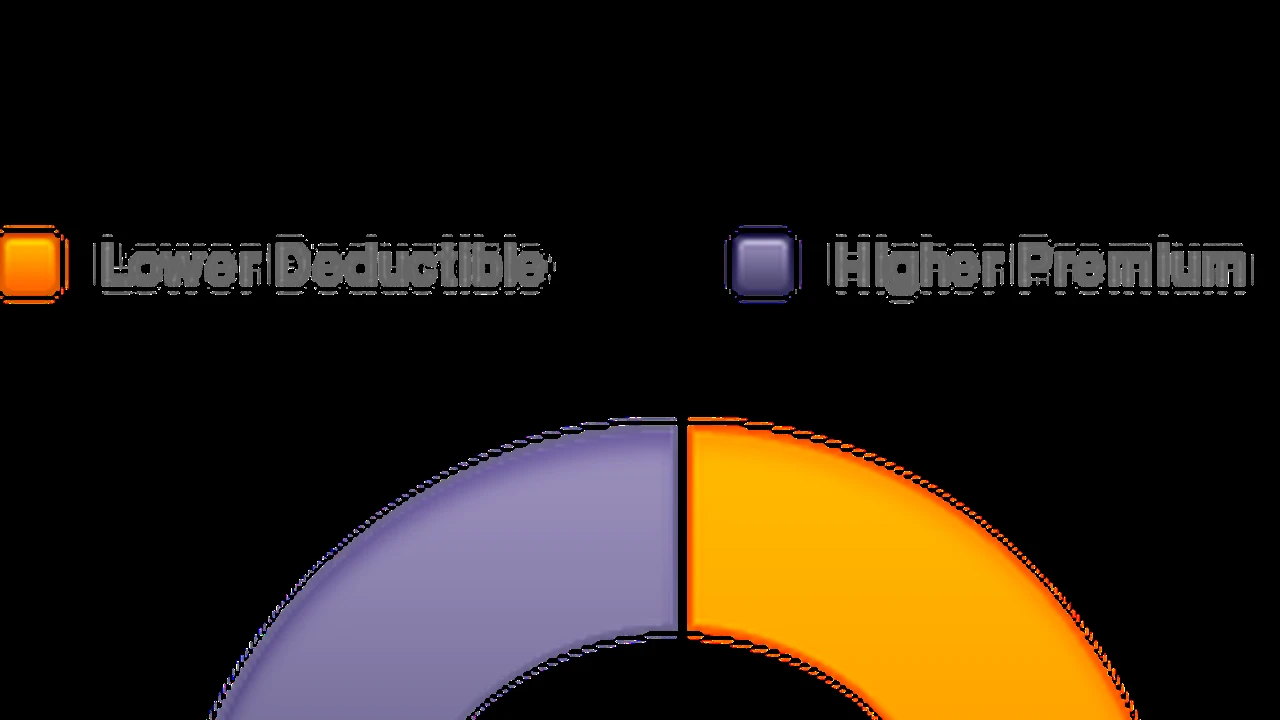

Why do deductibles exist? Well, they help keep insurance premiums lower. The higher your deductible, the less you'll pay each month (or year) for your insurance policy. Think about it: if you're willing to pay a larger chunk of the repair bill yourself, the insurance company takes on less risk, and they reward you with lower premiums. It's all about risk management.

Choosing the Right Deductible Level Balancing Cost and Coverage

So, how do you decide what deductible is right for you? This is where things get personal. You need to consider your financial situation, your driving habits, and your risk tolerance. Ask yourself these questions:

- How much can I comfortably afford to pay out-of-pocket in case of an accident? This is crucial. Don't choose a deductible so high that you'd struggle to pay it if you had to.

- How often do I drive, and what kind of driving do I do? If you drive a lot, especially in congested areas, your risk of an accident is higher.

- Am I a cautious driver, or do I tend to be a bit more...adventurous? Be honest with yourself!

Generally, deductibles range from $250 to $1,000 or even higher. A lower deductible (like $250) means you'll pay more in premiums but less out-of-pocket if you have a claim. A higher deductible (like $1,000) means you'll pay less in premiums but more out-of-pocket if you have a claim. It's a trade-off.

Example: Let's say you have a $500 deductible and you get into an accident that causes $3,000 worth of damage to your car. You'll pay the first $500, and your insurance company will pay the remaining $2,500.

Types of Car Insurance Coverage and Their Deductibles Collision vs Comprehensive

It's important to understand that deductibles typically apply to two specific types of car insurance coverage: collision and comprehensive. Let's break those down:

- Collision Coverage: This covers damage to your car if you hit another vehicle or object (like a tree or a fence), or if your car is damaged in a single-car accident.

- Comprehensive Coverage: This covers damage to your car from things other than collisions, such as theft, vandalism, fire, hail, or hitting an animal.

Liability coverage, which covers damage you cause to others, doesn't have a deductible. That's because it's designed to protect you from lawsuits and financial responsibility for injuries or damages you cause to someone else.

Real-World Scenarios How Deductibles Work in Different Accident Situations

Okay, let's walk through some real-world scenarios to see how deductibles work in practice:

Scenario 1: You're backing out of your driveway and accidentally bump into your neighbor's parked car, causing $1,000 worth of damage. You have collision coverage with a $500 deductible. You'll pay $500, and your insurance company will pay $500 to repair your neighbor's car.

Scenario 2: A tree falls on your car during a storm, causing $2,000 worth of damage. You have comprehensive coverage with a $250 deductible. You'll pay $250, and your insurance company will pay $1,750 to repair your car.

Scenario 3: Someone breaks into your car and steals your stereo, causing $300 worth of damage. You have comprehensive coverage with a $500 deductible. In this case, you'll have to pay the full $300 yourself, because the damage is less than your deductible.

Comparing Car Insurance Companies and Their Deductible Options Allstate vs State Farm vs Geico

Now, let's take a look at some popular car insurance companies and how they handle deductibles. Keep in mind that pricing and specific options can vary based on your location, driving history, and other factors, so it's always best to get a personalized quote.

- Allstate: Allstate typically offers deductible options ranging from $250 to $1,000. They are known for their strong customer service and a wide range of coverage options. Allstate's Drivewise program can offer discounts for safe driving habits.

- State Farm: State Farm also offers deductibles in the $250 to $1,000 range. They are known for their financial stability and strong local agent network. State Farm's Steer Clear program is designed for younger drivers and can help them save money on their insurance.

- Geico: Geico is often known for its competitive pricing and wide availability. They typically offer deductible options similar to Allstate and State Farm. Geico's mobile app makes it easy to manage your policy and file claims.

Product Recommendation and Comparison:

Let's consider a hypothetical scenario: You're a young professional living in a city, driving a relatively new Honda Civic. You want good coverage but are also budget-conscious.

Option 1: Allstate with a $500 Deductible

- Coverage: Comprehensive, Collision, Liability (100/300/100), Uninsured Motorist

- Deductible: $500 (Collision and Comprehensive)

- Estimated Annual Premium: $1200

- Pros: Strong customer service, potential discounts through Drivewise.

- Cons: Slightly higher premium compared to Geico.

- Usage Scenario: Ideal if you value customer service and are comfortable with a moderate out-of-pocket expense.

Option 2: Geico with a $1000 Deductible

- Coverage: Comprehensive, Collision, Liability (100/300/100), Uninsured Motorist

- Deductible: $1000 (Collision and Comprehensive)

- Estimated Annual Premium: $950

- Pros: Lowest premium, easy-to-use mobile app.

- Cons: Customer service may not be as personalized as Allstate or State Farm.

- Usage Scenario: Best for budget-conscious drivers who are comfortable with a higher out-of-pocket expense.

Option 3: State Farm with a $250 Deductible

- Coverage: Comprehensive, Collision, Liability (100/300/100), Uninsured Motorist

- Deductible: $250 (Collision and Comprehensive)

- Estimated Annual Premium: $1450

- Pros: Strong local agent network, good for building a long-term relationship with an agent.

- Cons: Highest premium.

- Usage Scenario: Suitable if you prefer a local agent and want a lower out-of-pocket expense.

Pricing Considerations:

The estimated annual premiums above are just examples. Actual prices will vary depending on your individual circumstances. It's always a good idea to get quotes from multiple companies to compare rates and coverage options.

Deductible FAQs and Common Misconceptions Debunked

Let's tackle some frequently asked questions and common misconceptions about car insurance deductibles:

- "If I'm not at fault in an accident, do I still have to pay my deductible?" Potentially, yes. If the at-fault driver is uninsured or underinsured, you may need to use your own collision coverage, which would require you to pay your deductible. However, your insurance company may try to recover your deductible from the at-fault driver's insurance company.

- "Can I change my deductible at any time?" Yes, you can usually change your deductible when you renew your policy. Some companies may allow you to change it mid-policy, but there might be restrictions.

- "Is it always better to have a lower deductible?" Not necessarily. A lower deductible means higher premiums. You need to weigh the cost of the premiums against the potential out-of-pocket expense.

- "My car is old. Should I even have collision or comprehensive coverage with a deductible?" That's a valid question. If your car's value is low, the cost of collision and comprehensive coverage might not be worth it. Consider dropping these coverages if the premiums are high relative to the car's value.

Tips for Saving Money on Car Insurance Deductibles and Premiums

Here are a few tips to help you save money on car insurance:

- Shop around: Get quotes from multiple insurance companies.

- Increase your deductible: A higher deductible can significantly lower your premiums.

- Bundle your insurance: Insure your car and home with the same company for a discount.

- Maintain a good driving record: Avoid accidents and traffic violations.

- Take advantage of discounts: Ask about discounts for safe driving, good student status, military service, and more.

- Review your coverage annually: Make sure you have the right coverage for your needs and budget.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)