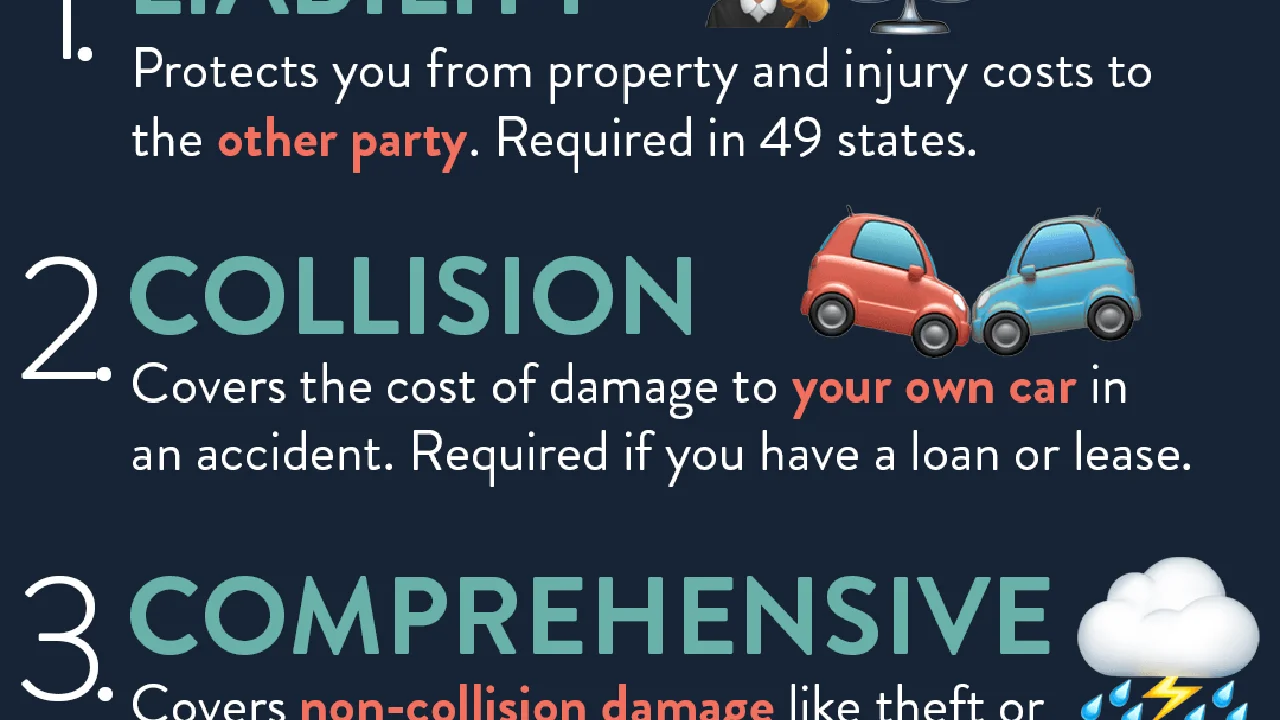

Uninsured and Underinsured Motorist Coverage Explained

What is Uninsured Motorist (UM) Coverage and Why You Need It

Okay, let's talk about something that might not be the most exciting topic, but it's definitely one of the most important when it comes to car insurance: Uninsured Motorist (UM) coverage. Imagine this: you're driving along, minding your own business, and BAM! Someone hits you. Not fun, right? But what if that someone doesn't have insurance? Or worse, they don't even have enough insurance to cover all the damage to your car and your medical bills? That's where UM coverage comes to the rescue.

Think of Uninsured Motorist coverage as your safety net when you're involved in an accident with a driver who either doesn't have insurance at all or doesn't have enough. It helps cover your medical expenses, lost wages, and even pain and suffering. Without it, you could be stuck paying out of pocket for everything, which can be a huge financial burden.

Different states have different requirements for UM coverage. Some states require it, while others don't. But even if your state doesn't require it, you should seriously consider getting it. Trust me, it's better to be safe than sorry.

Understanding Underinsured Motorist (UIM) Coverage: Your Second Line of Defense

Now, let's talk about Underinsured Motorist (UIM) coverage. This is similar to UM coverage, but it kicks in when the at-fault driver does have insurance, but their coverage limits aren't high enough to cover all your damages. So, let's say you have $50,000 in medical bills and your car is totaled, but the other driver only has $25,000 in liability coverage. Your UIM coverage can step in to cover the remaining $25,000 (or however much your policy covers).

UIM coverage is just as important as UM coverage. Medical bills can add up quickly, and you don't want to be left footing the bill because someone else didn't have enough insurance. It's important to understand the difference between UM and UIM coverage and to make sure you have adequate coverage for both.

Uninsured Motorist Property Damage (UMPD): Protecting Your Vehicle

Most people think about medical bills when they think about uninsured/underinsured coverage, but what about your car? Uninsured Motorist Property Damage (UMPD) coverage is designed to cover the damage to your vehicle if you're hit by an uninsured driver. It's usually subject to a deductible, but it can save you a lot of money if your car is damaged or totaled.

Not all states offer UMPD coverage, and in some states, it might be included as part of your collision coverage. Check with your insurance company to see what's available in your state and what makes the most sense for your needs.

Cost of Uninsured and Underinsured Motorist Coverage: Is it Worth the Price?

Okay, let's be real. Adding UM and UIM coverage to your car insurance policy will increase your premium. But the question is: is it worth the price? In my opinion, absolutely. The cost of UM and UIM coverage is relatively low compared to the potential financial devastation you could face if you're involved in an accident with an uninsured or underinsured driver.

The exact cost will depend on several factors, including your state, your driving record, and the coverage limits you choose. But typically, you can add UM and UIM coverage for just a few extra dollars per month. Think of it as an investment in your financial security.

Comparing UM/UIM Coverage from Different Insurance Companies: What to Look For

Not all UM/UIM coverage is created equal. Different insurance companies offer different coverage options and different prices. Here's what you should look for when comparing UM/UIM coverage:

- Coverage Limits: Make sure the coverage limits are high enough to adequately protect you. Consider your assets and potential medical expenses when choosing coverage limits.

- Stacking vs. Non-Stacking: In some states, you can "stack" your UM/UIM coverage if you have multiple vehicles on the same policy. This means you can combine the coverage limits from each vehicle to increase your overall coverage. Check with your insurance company to see if stacking is available in your state.

- Price: Of course, price is a factor. Get quotes from multiple insurance companies and compare the prices. But don't just choose the cheapest option. Make sure you're getting adequate coverage for a reasonable price.

- Reputation: Check the insurance company's reputation. Read reviews online and see what other customers have to say. You want to choose a company that's known for paying claims fairly and promptly.

Real-Life Scenarios: When UM/UIM Coverage Saved the Day

Let me tell you a few stories to illustrate the importance of UM/UIM coverage. These are based on real-life situations, with some details changed to protect privacy:

- Scenario 1: The Hit-and-Run: Sarah was driving home from work when she was rear-ended by another car. The other driver sped off, leaving Sarah with a totaled car and a neck injury. Thankfully, Sarah had UM coverage, which covered the cost of her medical bills and the replacement of her car. Without UM coverage, she would have been stuck paying for everything out of pocket.

- Scenario 2: The Underinsured Driver: John was seriously injured in a car accident caused by another driver. The other driver had insurance, but their coverage limits were only $25,000. John's medical bills alone exceeded $100,000. John had UIM coverage, which covered the remaining $75,000 in medical bills. Without UIM coverage, he would have been facing a mountain of debt.

- Scenario 3: The Motorcycle Accident: Maria was riding her motorcycle when she was hit by an uninsured driver. Maria suffered severe injuries, including a broken leg and a concussion. Maria had UM coverage, which covered her medical bills, lost wages, and pain and suffering. Without UM coverage, she would have been in a very difficult financial situation.

Specific Product Recommendations: UM/UIM Coverage Options from Top Insurers

Okay, now let's talk about some specific insurance companies and the UM/UIM coverage options they offer. Keep in mind that coverage availability and pricing can vary depending on your location and individual circumstances. It's always best to get a personalized quote.

State Farm Uninsured Motor Vehicle Coverage

State Farm is a well-known and reputable insurer with a wide range of coverage options. Their UM coverage is pretty comprehensive, and they offer different levels of coverage to suit your needs. They also offer UMPD.

- Pros: Strong financial stability, good customer service, wide range of coverage options.

- Cons: Can be slightly more expensive than some other insurers.

- Use Case: Ideal for families looking for comprehensive coverage from a trusted insurer.

- Price: Adding UM/UIM coverage can typically add $10-20 per month to your premium, depending on your coverage limits.

Geico Uninsured Motorist Coverage

Geico is known for its competitive prices and user-friendly online platform. Their UM/UIM coverage is pretty standard, but they offer a variety of discounts that can help you save money.

- Pros: Competitive prices, easy online access, various discounts available.

- Cons: Customer service can be inconsistent at times.

- Use Case: A good choice for budget-conscious drivers who are comfortable managing their policy online.

- Price: You can often find UM/UIM coverage through Geico for around $8-15 per month.

Progressive Uninsured and Underinsured Motorist Coverage

Progressive offers a "Name Your Price" tool, which allows you to customize your coverage to fit your budget. They also offer UM/UIM coverage, and they have a good reputation for handling claims.

- Pros: "Name Your Price" tool, good claims handling, 24/7 customer service.

- Cons: Can be difficult to compare prices with other insurers.

- Use Case: Suitable for drivers who want more control over their coverage options and budget.

- Price: The price of UM/UIM coverage with Progressive will vary greatly depending on your "Name Your Price" selection.

UM/UIM Coverage: Stacking vs. Non-Stacking

Let's dive a little deeper into the concept of "stacking" UM/UIM coverage. Stacking, where it's allowed, can significantly increase your protection. Here's the breakdown:

What is Stacking?

Stacking allows you to combine the UM/UIM coverage limits from multiple vehicles on the same policy, or even from multiple policies, to increase your overall coverage. For example, if you have two cars on your policy, each with $100,000 in UM coverage, stacking would allow you to have a total of $200,000 in UM coverage.

Stacking vs. Non-Stacking

In states that allow stacking, you'll typically have the option to choose between stacking and non-stacking coverage. Non-stacking coverage means that you can only access the UM/UIM coverage limits for the vehicle you were in at the time of the accident.

Benefits of Stacking

- Increased Coverage: The most obvious benefit is that you have more coverage available in the event of a serious accident.

- Better Protection Against High Medical Bills: Stacking can be particularly beneficial if you live in a state with high medical costs.

Considerations

- Availability: Stacking is not allowed in all states.

- Cost: Stacking coverage typically costs more than non-stacking coverage.

UM/UIM Coverage and Motorcycle Insurance

Motorcycle riders are particularly vulnerable in accidents, making UM/UIM coverage even more crucial. Here's why:

- Higher Risk of Injury: Motorcycle riders are more likely to be seriously injured in an accident than drivers of cars.

- Limited Protection: Motorcycles offer less physical protection than cars.

- Higher Medical Bills: Serious injuries often result in high medical bills.

If you're a motorcycle rider, make sure you have adequate UM/UIM coverage to protect yourself in the event of an accident with an uninsured or underinsured driver.

Filing a UM/UIM Claim: What to Expect

If you're involved in an accident with an uninsured or underinsured driver, you'll need to file a UM/UIM claim with your own insurance company. Here's what you can expect:

- Report the Accident: Report the accident to your insurance company as soon as possible.

- Gather Information: Gather all relevant information, including the police report, medical records, and repair estimates.

- Cooperate with the Insurance Company: Cooperate with the insurance company's investigation.

- Negotiate a Settlement: Negotiate a fair settlement with the insurance company. You may need to hire an attorney if you're unable to reach a settlement.

How to Lower Your Car Insurance Rates: Tips and Tricks

While UM/UIM coverage is essential, you probably still want to save money on your overall car insurance premium. Here are some tips:

- Shop Around: Get quotes from multiple insurance companies.

- Increase Your Deductible: A higher deductible will lower your premium.

- Maintain a Good Driving Record: Avoid accidents and traffic violations.

- Take a Defensive Driving Course: Some insurance companies offer discounts for completing a defensive driving course.

- Bundle Your Insurance: Bundle your car insurance with your home insurance for a discount.

- Ask About Discounts: Ask your insurance company about all available discounts.

The Future of UM/UIM Coverage: What to Watch For

The landscape of car insurance is constantly evolving. Here are some trends to watch for in the future of UM/UIM coverage:

- Increased Coverage Limits: As medical costs continue to rise, we may see an increase in the recommended UM/UIM coverage limits.

- Changes in State Laws: State laws regarding UM/UIM coverage are subject to change.

- Technological Advancements: New technologies, such as autonomous vehicles, could impact the need for UM/UIM coverage.

Stay informed about the latest developments in car insurance to ensure you have the coverage you need.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)